What are the challenges facing charities participating in the local government pension scheme? David Davison of Spence & Partners shares new research that lifts the lid on the financial impact the schemes have on the UK charity sector.

In supporting members who participate in the local government pension scheme (LGPS) it has always been difficult to obtain information for the sector as a whole and also to allow charities to assess their position.

As a corporate sponsor of CFG and having provided support in this area in the past, we wanted to look to address that and so have now published ‘Research on Charities in LGPS’ to hopefully provide valuable information to charities.

We started by analysing the actuarial valuation reports for the 99 schemes across the UK to identify which charities participated.

We refined this information by removing non charities and duplicates for employers which left us with a pool to 608. However, from these we were only able to identify 208 where full FRS102 pension disclosures and comprehensive accounting information was included in the charity accounts.

Whilst clearly we would have preferred to have access to a greater number of complete records we believe the population identified is large enough to provide a good indication of trends and to allow us to draw some conclusions.

The key findings of the research were:

- The accounts were compiled by well over 100 different audit firms. A huge array of accounting design and terminology was used within the disclosures and I’m sure we would all welcome an increased level of consistency of approach to make these important figures more accessible for users.

- The estimated funding position in 2021 on an ‘on-going’ basis suggested that overall the 208 employers were fully funded on this basis. However, the funding rate fell to 79% on an FRS basis with a deficit of around £1bn and 69% on a cessation basis with the deficit rising to around £1.8Bn. Interestingly the funding position on this basis for individual employers ranged from 20% to 150%.

- Around 20% of the employers accounted for approximately 85% of the deficit which highlights how significant a problem this is for some charities and something which could potentially threaten their continuing existence.

- Based upon a full population of participating charities the sector could potentially, in 2021, have total liabilities in excess of £15Bn and a cessation deficit in excess of £5Bn.

- The cessation deficit of £1.8bn represented around 22% of adjusted total reserves but 63% of unrestricted reserves and around 39% of total income. Again however, there was a wide distribution across employers in this analysis with around half of employers showing a negative against unrestricted reserves but only around 20% with a material deficit.

- Whilst there is a lot of focus from Funds on Covenant research, considering the financial strength of charities in relation to their accrued liabilities, there has been much less focus on the risk of building additional liabilities and the risk that entails both for charities and the Funds as a whole. Employer contributions for the 208 employers were around £110m which would suggest across the whole sector would be in excess of £300m. Employer contributions represented around 33% of movement in net funds while the accruing cessation liability would represent around 60% to 75% of this figure. Again, this analysis suggests that this metric highlights a significant financial risk for the bottom 20% of charities.

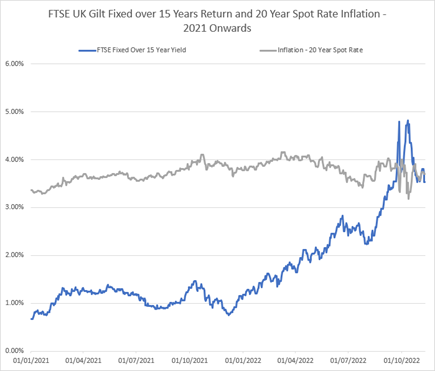

Given that the figures were compiled using available financial information in 2021 we also decided to roll forward the analysis to November 2022. The cessation position is primarily driven by gilt yields and inflation and the table below highlights the movements in these since the start of 2021.

The table highlights that gilt yields have risen very dramatically, particularly since April 2022 and higher gilt yields place a lower value on the accrued liabilities.

Whilst short-term inflation has spiked the expectation on longer them inflation has been fairly static. This has therefore presented a very positive improvement in the LGPS cessation funding position.

Our analysis suggested that updating the results to end November 2022 saw the cessation deficit fall from the £1.8bn figure to around £200m (assuming an estimated 10% fall in asset values which is consistent with what we’ve witnessed in engagements with Funds).

What we have also witnessed through 2022 is that some funds are moving away from the purely gilts-based cessation calculation model and are instead adopting a probability model which assumes an 80% or 90% probability of success that the deficit will be funded over an agreed funding period.

This approach allows for some level of future return over gilts which therefore tends to reduce the cessation liabilities. This can be by 10%-30%, depending upon the duration of the liabilities, and therefore materially reduce any cessation debt payable.

In our view this direction of travel away from a pure gilts-based methodology is more equitable and hopefully over time will become the default cessation approach for Funds.

These changes in market conditions between April 2022 and the end of 2022 have been dramatic and will have changed the deficit position for all charities in LGPS very significantly reducing cessation/exit deficits.

Particularly for charities that are closed to new entrants and therefore who are inevitably working towards a cessation they need to actively consider if they should be taking actions now to bring that cessation timescale forward.

Access the full research paper.