As expected, the Chancellor’s Spring Statement did not introduce any new policy measures, sticking to her promise to only hold one fiscal event per year. The announcement, therefore, does not substantively change the financial situation for charities.

Economic outlook

It is worth noting that the OBR’s forecast does not take into the account the financial turmoil caused by the ongoing war in the Middle East, which could have a significant impact on inflation if the conflict persists. Suffice to say there is much uncertainty with any of these predictions.

With demand still high, financial pressures unabating and public finances tight, many organisations are heading into another difficult year with tough choices ahead.

The OBR has downgraded growth next year and expects unemployment to rise further. That combination risks increasing pressure on charitable services at the very moment many charities are least able to absorb it.

The forthcoming Autumn Budget will be a crucial opportunity to provide relief for charities. We will be working with sector partners to deliver meaningful change to help ease the financial burden many charities find themselves in.

Please find more details on the key information from the OBR forecast below:

OBR forecast and economic data

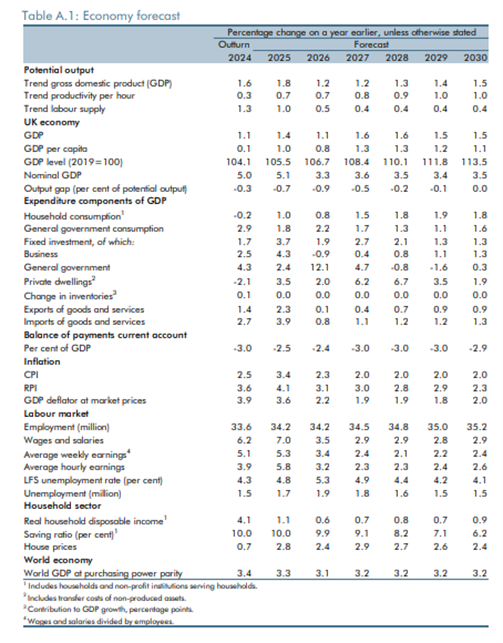

Real GDP growth and real GDP per person

A point latched on to by the Opposition is the slight reduction in forecasted GDP growth: 'real GDP growth is expected to slow from 1.4 per cent in 2025 to 1.1 per cent in 2026. The latter is 0.3 percentage points lower than in November, reflecting weaker-than-expected GDP outturns in late 2025.’ Although growth is set to increase after that ever so slightly.

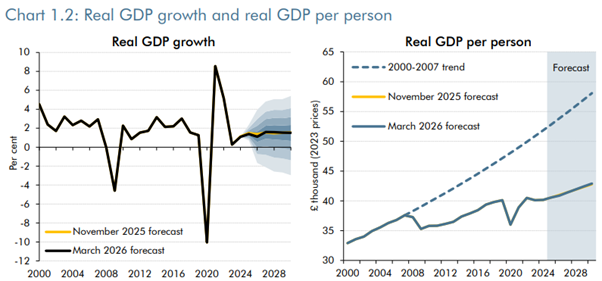

CPI Inflation

The OBR projects 'CPI inflation will fall from 3.4 per cent in 2025 to 2.3 per cent in 2026, and 2.0 per cent from 2027 onwards’, reaching the 2% target in late 2026.

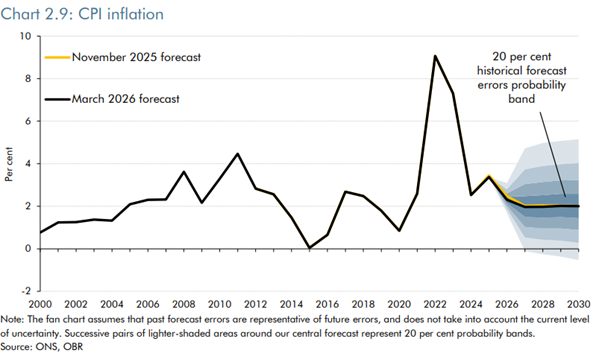

Public spending as a share of GDP

Public spending is forecast to rise to 44.9% of GDP over the next quarter before gradually declining to 44.3% by 2030-31.

Departmental expenditure limits are expected to rise as a share of GDP from 20.6% of GDP in 2024-25 to 21.3% of GDP in 2027-28 and then fall to 20.7% of GDP in 2030-31.

These are essentially identical to the November 2025 forecasts.

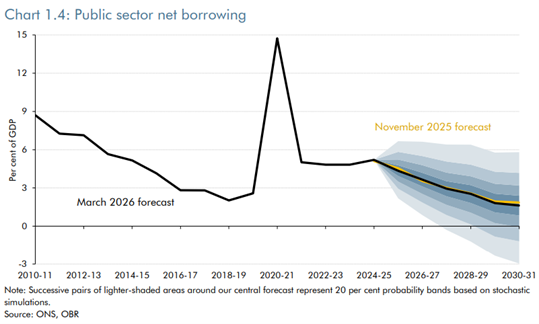

Public sector net borrowing

Borrowing as a share of GDP is projected to fall from 5.2% last year, to 4.3% this year, and then decline to 1.6% of GDP in 2030-31. A minor change in the pace of the decrease from the November forecast which had it set to decline to 1.9% in 2030-31, due to an 'improved receipts forecast'.

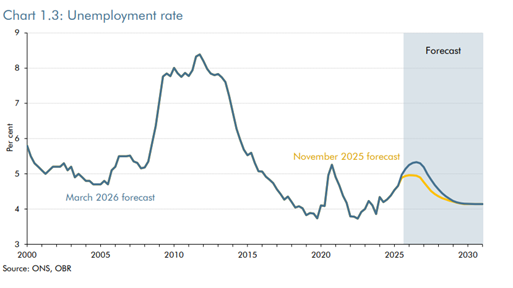

Unemployment rate

The previous peak of near 5% is estimated to be slightly surpassed, now reaching 5.33%, however the 'equilibrium rate of 4.1%’ by 2030 remains the same.

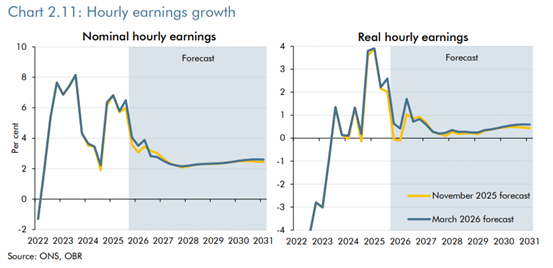

Nominal and real earnings growth

Little changes to wage growth, as the OBR states: 'Nominal weekly wage growth is expected to slow to around 3.5% in 2026 and then average 2.25% a year, broadly in line with our November forecast.'

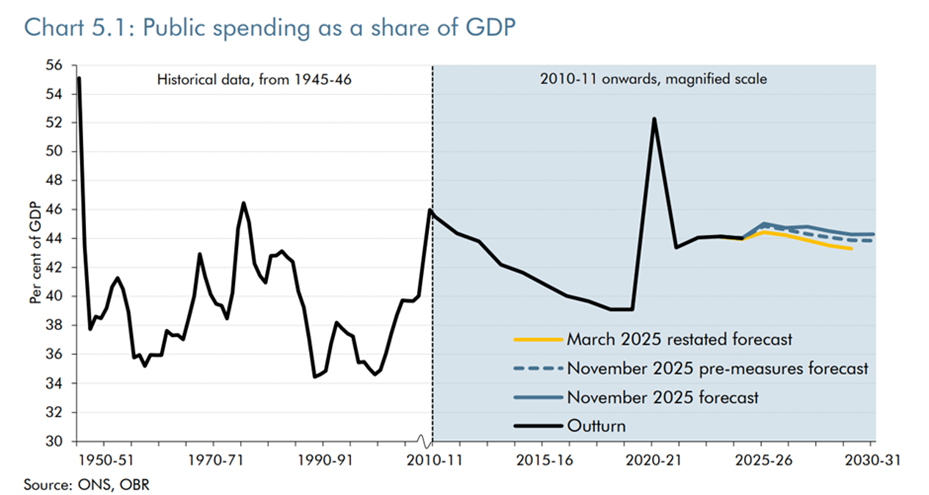

TABLE: Economy Forecast