Pension schemes haven't escaped recent political and economic turmoil, so it's time to revisit your organisation's pensions strategy. Ed Symes and Richard Soldan from LCP explain why.

The disastrous 'mini budget' highlighted that charities need to pay close attention to the impact of financial markets on their defined benefit pension schemes.

Whilst many organisations will have seen a significant improvement in their defined benefit funding position, some charities’ pension schemes will have been badly hit by the recent turmoil.

Now that the dust has settled, charities need to revisit their pensions strategy. If the position has improved there are likely to be great opportunities to capture the good news and reduce future risk; if the funding level has worsened, charities will need to understand why, and take action.

It will also be important to consider the potential impacts of the forthcoming new funding regulations and, if a charity uses a pension scheme run by TPT, to consider the possible impact of their upcoming court case and benefit review. More on this below.

Most favourable opportunities to reduce pension risk for many years?

The 'mini-budget' caused an upheaval in bond markets and the shortest prime ministerial stay in UK history.

Ironically, it has also resulted in many defined benefit pension schemes seeing their highest funding levels and lowest costs to exit for many years.

This is because we have been left with higher expectations for future government borrowing rates. All else equal, these higher long-term interest rates reduce the value placed on pension scheme liabilities, as an expectation of higher future investment returns means pension schemes need to hold less money now in order to pay the pensions to their members in the future.

This is likely to reduce deficits in many cases and to reduce both 'buyout' premiums charged by insurers for taking on a charity’s pension liabilities and exit debts calculated by multi-employer schemes like the Local Government Pension Scheme (LGPS).

While expectations for long-term interest rates have fallen back somewhat in the last couple of weeks (we are writing this on 1 November 2022), we still expect some great opportunities to reduce risk and exit defined benefit pension liabilities for good.

As an example, one charity we work with has recently secured all its DB pension liabilities with an insurer at a much lower cost than expected – a great outcome for both the charity and the pension scheme members.

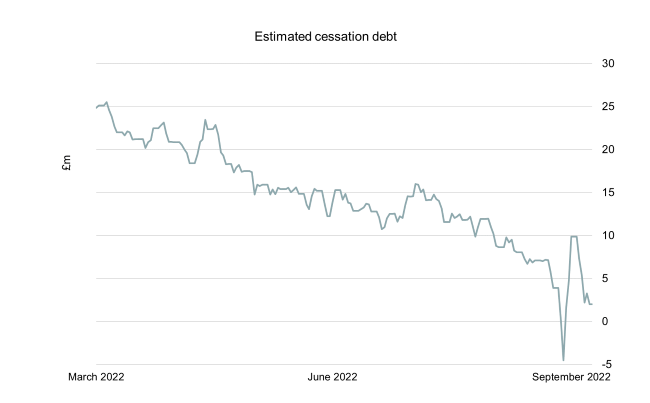

Similarly, the below chart shows how the estimated exit debt for a not-for-profit organisation in one of the LGPS funds has fallen from £25m to almost £nil over the last six months:

But some schemes are under pressure following recent events

It’s not all good news though. Some pension schemes were not able to cope with such unprecedented volatility in interest rates and were forced sellers of some investments at the bottom of the market.

Those who found themselves in this unfortunate position will have seen their funding position worsen, possibly significantly.

Whether this impacts you is down to whether your 'liability driven investment' (LDI) arrangements were able to cope with the rapid rise in bond yields or whether these strategies failed – some schemes are nursing significant losses.

If you are in this position, you need to revisit your scheme’s investment strategy, review your long-term planning and see how pension contributions may need to change to reflect the new situation.

New funding regulations

Lurking in the future is a major overhaul of the defined benefit funding and investment regulations.

The Pensions Regulator’s formal consultation on its first draft of the new regulations ended on 17 October 2022 and, if implemented as planned, will result in a much more rigid regime with much less flexibility.

This could end up with more prudent funding targets and higher contributions which could ultimately be unaffordable for many charities.

We know that currently for-profit organisations have deficit recovery plan lengths of on average seven years, versus nine years on average for a not-for-profit sponsor. These are the results of our Freedom of Information request.

If the new funding regime were to mean that charities had to align their deficit recovery plans to the shorter period of seven years (or even less) this could result in a 25% average increase to deficit contributions.

TPT benefit review and court case

TPT Retirement Solutions, which runs the pension schemes used by many charities, are currently performing a benefit review.

They have concerns that some historical changes to their pension schemes have not been implemented correctly, and they are asking the High Court to decide the correct interpretation.

If the Court rules against TPT, this could add many millions of pounds to the liabilities of those organisations sponsoring TPT schemes. This is potentially a huge issue for some charities.

If you are in this position it will be important to understand the scale of any potential additional liabilities, and to ensure the strategy for your scheme takes account of the risk that those liabilities may need to be paid for, either through extra investment returns (potentially meaning a higher risk strategy) or through cash contributions – which would be highly unwelcome in the current environment.

What should charities do next?

Charities should proactively ask for an up-to-date estimate of their funding position for each defined benefit scheme they participate in, and use that information to consider their options to reduce risk and cost.

Those who sponsor a TPT pension scheme should also be proactively engaging with TPT on the benefit review and we are working with a number of charities in the sector on this topic.

If you do have a pleasant surprise on your funding position then you should be considering actively how to reduce risk and/or exit your liabilities while times are good.

If your scheme funding position is worse, or your scheme has been forced to change its investment strategy through the recent turmoil, it will be really important to review the strategy to reflect the best balance of risks and future returns for your organisation.

If there is limited cash available to top up the funding position, then we would suggest looking at non-cash funding options, such as security over fixed assets like a head office.

Either way, now is definitely the time to act!

If you would like to discuss your situation, please email Ed Symes or Richard Soldan.

Use of LCP's work

This generic note should not be relied upon for detailed advice or taken as an authoritative statement of the law. If you would like any assistance or further information, please contact the partner who normally advises you or Ed or Richard at the contact details above. While this document does not represent our advice, nevertheless it should not be passed to any third party without our formal written agreement.