Recent research by CFG shows that charity audits are becoming ever more costly and complex. At the same time, auditing is fast-evolving and needs to attract more talent. What, if anything can be done about it? Is it time for a rethink on audit? Sam Burne James investigates…

Phrases like “I feel their pain”, or the same sentiment expressed in different words, pop up frequently both when asking CFG members about their auditors, and auditors about their charity clients.

Auditors are subject to increasing regulatory demands, on top of internal budget and talent pressures, meaning that carrying out a charity audit is harder, longer and most costly.

Charities, meanwhile, must absorb these costs and the rising demands on the diaries of their finance teams, on top of frequent challenges finding a suitable or willing auditor.

A strain and a drain?

Neil Goulder is Finance Director of charity arts production company Artichoke. The cost of its audit rose by nearly 25% this year, which he calls “substantial for something that creates no added value for us.”

Goulder acknowledges that even if Artichoke itself doesn’t gain anything from its audit, funders take “a lot of reassurance that the risk… is minimised if the recipient is audited”. As such, he says the charity would not forego an audit, even if released from that regulatory requirement.

Other charity finance leaders feel similarly. Jeff Green of the British and Irish Association of Zoos and Aquariums (BIAZA), which is about to be audited for the first time, says: “I don’t think it will tell us anything we don’t know, but ultimately having someone look is a good thing.”

Green says that a “frustration” for BIAZA is that its income is below England and Wales’ £1m charity audit threshold, but above the £500,000 stipulated in Scotland. It is unclear exactly how many charities are caught by this cross-border variation, but BIAZA won’t be alone.

Audit’s increasing drain on staff time is a frustration for Angela Spreadbury, Director of Finance and Administration at the SS Great Britain Trust, a museum in Bristol.

She explains: “While my team and I are quite happy for people to give us scrutiny,” she says, “it would be great if we could reduce the amount of time it takes… [especially] having to provide huge levels of evidence for absolutely everything.”

Spreadbury adds that the cost of getting audited “has probably more than doubled” in the last decade.

Rising costs

A recent CFG survey of 250 members found that 43% are paying between £10,000 and £25,000 for audit, while around a fifth are paying more.

Another fifth pay less than £5,000, although market trends suggest they may struggle to keep fees that low for long.

While some charities report instances of auditors quoting uncompetitive rates in what they know is a seller’s market, there is also an understanding that fees need to go up.

Says Spreadbury: “I do feel auditors’ pain, frankly – they are having to work very hard because of the regulations and additional requirements that have been layered on, and also because charities are very complex.”

Charity accounting specialists said they understand these concerns. Sudhir Singh, National Head of Not-For-Profit and an audit partner at MHA, says he hoped charity auditors will "try to avoid passing on extra costs to their clients”, but that increasing complexity has “unfortunately” put pressure on fees.

In the long term, he adds, audit has become a more specialist profession, creating a squeeze in the market.

“Back when I trained, everyone working in general practice in an accounting firm could be an auditor, now it’s a smaller, highly specialist practice discipline,” Singh comments.

Naziar Hashemi, head of social purpose and non-profits at Crowe, accepts that the market “is very tight” and that some charities feel audit is “a statutory nuisance”.

Says Hashemi: “Whilst all auditors strive to deliver quality, the challenge with increasing regulations and sanctions is that it will make audit unattractive as a career choice for young people.”

Smoothing the path

What, then, can charities and auditors do to ensure the process is as pain-free as possible, and to see where value can be added during it?

“Ask your auditor for plenty of guidance before an audit happens about how to make the process run as smoothly as possible,” suggests Singh.

A charity can also pick its auditor’s brain, he says, for “information and opinions on a range of matters… [seeking] valuable insights that will support the charity to build healthy finances and governance”.

While some charity finance professionals have not found that this is offered, Singh counters: “I would suggest that if your auditor isn’t forthcoming with ways to add value, then you might not have the right auditor.”

Hashemi warns that this value-add is under threat from a consultation (running to 31 October) on the Financial Report Council’s Ethical Standard.

Currently, external auditors may perform additional, non-audit services, but the definition of which services fall under that definition could be narrowed, Hashemi warns.

This could be “problematic for charities, especially those without the resources and time to procure these services from an alternative firm”.

The perfect match

Auditor selection is something which Richard Barker, education charity Goodenough College’s Director of Finance and Resources, has experience.

The college recently moved its audit to another firm, while a charity of which Barker is trustee recently re-tendered, reappointing the incumbent.

“Both exercises were very valuable, but it is quite a lot of work, in particular you need to do a lot of briefing of potential providers,” Barker says. You can read his full advice on tendering here.

While charities like Goodenough College, with annual incomes of more than £10m, might look like an attractive client to auditors, some smaller charities report struggles finding an auditor .

One charity reports losing its auditor after the firm concluded that the business wasn’t worthwhile. Another was “essentially ghosted” by its auditor, nearly missing its filing deadline as a result.

Staffing shortages appeared to be the particular problem that led to that auditor being slack, but it doesn’t seem unreasonable to assume that its larger, private sector clients might not have experienced the same.

Alex Russell, head of audit and assurance strategy at the Institute of Chartered Accountants in England and Wales (ICAEW), says: “In the current unprecedented circumstances, when firms have more requests for audit than they can service, they have to be selective.”

The audit thresholds for non-charitable companies don’t do the third sector any favours. In the private sector, audit is a requirement for companies with two (or more) of the following: turnover in excess of £10.2m, assets worth more than £5.1m, or 50 or more staff. This makes many charities small clients for the audit sector.

Crossing the threshold

The Office of the Scottish Charity Regulator (OSCR) told CFG that if a charity missed its filing deadline because of challenges finding an auditor, that it would be “proportionate in response, appreciating the difficulties experienced”.

The Charity Commission for England and Wales (CCEW) did not directly respond to this question, but pointed out that it regulates on a risk-based, case-by-case basis.

Market challenges notwithstanding, these regulators, plus their Northern Ireland counterpart, are at the mercy of laws set by their respective Governments.

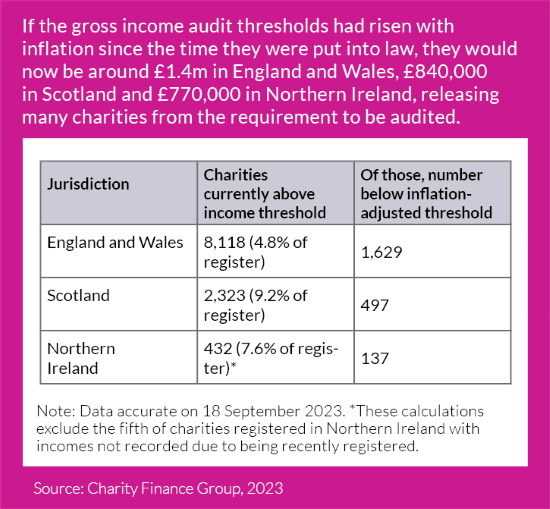

While charity finance leaders respect the need to comply with those laws, many feel thresholds are simply too low, not least because of the impact of inflation: the number of Scottish charities exceeding £500,000 income has grown from 6% of OSCR’s register in 2008 to 9% today.

Russell from the ICAEW suggests that “one possible avenue worthy of exploration” is the Less Complex Entity (LCE) Auditing Standard.

Due for UK adoption this year, this could reduce the burden for charities not far above the threshold. CFG and CCEW are among the stakeholders now liaising with ICAEW on this.

Alongside a straightforward raising of thresholds, CFG is making the case with Governments and regulators for it to rise to £1.5m across the UK.

Some interviewees suggested creative alternatives, such as charities above the threshold only having to do an audit some years, or having a threshold based on number of transactions, recognising the fact that income itself is not directly proportional to level of complexity.

Pushing through the pain

Commentators also recognise that raising thresholds is not without its challenges, for example if funders’ risk appetites change when looking at non-audited potential grantees.

An OSCR spokesperson acknowledges that it would put more demand on independent examiners, who “are still in short supply”.

This problem is compounded by concerns raised by one independent examiner about his peers. On taking on a new charity client, he saw that its governing document required it to be audited, a fact that had clearly eluded multiple previous independent examiners, raising questions about the robustness of this form of external scrutiny.

It’s an uneasiness shared by the Charity Commission. In 2019, it highlighted concerns about both the quality of both auditors and independent examiners, and created a resource designed to improve standards.

CFG’s Director of Policy and Communications Clare Mills says: "On behalf of and alongside our members, we will continue to make representations about the proportionality of the audit process".

Across the sector, however, there is little confidence in the imminent overhaul or UK-wide standardising of those laws, and Mills adds: “Finding ways to ensure audit regulation is proportionate to the work involved is, unfortunately, not something that is likely to happen easily or quickly, due to the complex nature of financial and charity regulation.”

Many in both the charity and audit sectors will feel that reform cannot come soon enough. Sadly, nobody should be holding their breath.

Meanwhile, charity finance professionals know that their only option is to continue to push through the pain and make the best of a less than ideal environment. Overcoming adversity is, after all, very much in the nature of the charity sector.