On 4 February, the Bank of England delivered its Monetary Policy Report. CFG's Policy Manager Richard Sagar summarises the main findings.

The big news from the BoE monetary policy committee was that interest rates remained unchanged at 0.75% with a vote of 7 to 2 voting against a change. Many had predicted that there would be a cut, due to weak economic data, but there seems to have been a wait-and-see approach. With some evidence that the economy may be starting to pick up, which has meant temporarily there has been a pause of changing the rate. As Governor Mark Carney was reported to say ‘So far… good enough’. But aside from the decision not to change interest rates there are a number of interesting takeaways within the Bank’s Monetary Policy Report.

Growth has slowed in the UK economy

As the chart below indicates 2019 was a notably bad year for growth in the UK economy. In fact, It was at its lowest levels since the great recession. With the most recent quarterly growth figures showing that the UK economy didn’t grow at all in Q4 2019. There are numerous explanations offered for this, including business uncertainty due to Brexit.

Things look better in the medium term

While looking at last year’s economic data, you might be tempted to draw a pessimistic conclusion about the future. But there are early signs that economic growth is picking up. This is indicated in the Bank’s medium term forecasts with growth increasing year on year, with its forecast to be at 2% in Q1 2023. With a slight increase in inflation over this period, but still within, or just above the Bank’s target of 2%.

Productivity issues

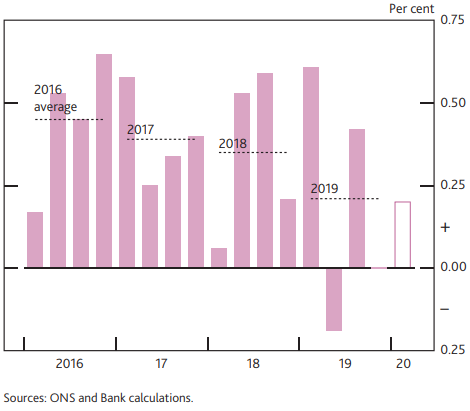

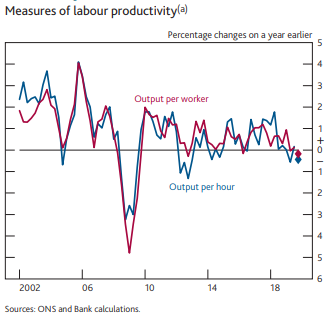

But as we can see from the table above, there is expected to be a corresponding increase in inflation. The monetary policy committee has judged that there is a margin of spare capacity in the economy, due to such low productivity. In fact as the graph below demonstrates, productivity growth is expected to be below zero in the year to 2019 Q4.

There’s good evidence to suggest that this is in part due to the impact that planning for Brexit has had on productivity growth, as the chart below indicates.

But a decline in productivity has also been a global phenomenon, with all countries in the G8 experiencing similar problems, so clarity on Brexit may not resolve this major concern with the UK economy.

Growth in real wages

There has been some good news on pay, as there has been notable growth in real wages for some time. One might think that this would be good news for donations to charity, but as the recent analysis by CAF has demonstrated, donations to charities have barely changed, and in fact their evidence suggests that fewer people are now giving.

Implications for public finances

FT has pointed out that if the BoE forecast comes to pass, then it could leave a £12 million black hole in the public finances. This would not give the chancellor the fiscal wiggle room to meet the Conservative party’s election pledge to end austerity and invest in the new Northern and Midlands' constituencies that were gained from Labour.

With this in mind, the chancellor can either meet his pledge to end austerity, or raise taxes to pay for it. It goes without saying that for political reasons neither of these is particularly palatable.

It’s why alongside other charity membership bodies we have been calling for the government to reinvest in local communities and end the reinvest in local authorities.